The AIER Everyday Price Index (EPI) rose 0.52 percent to 284.8 in January 2024. It was the largest percent change since August 2023, and brings the year-over-year EPI change to 1.45 percent.

AIER Everyday Price Index vs. US Consumer Price Index (NSA, 1987 = 100)

Among January 2024 EPI constituents, the largest monthly price increases occurred in the housing fuels and utilities; audio discs, tapes, and other media; and postage and delivery services categories. The largest price declines occurred in prescription drugs, intracity transportation, and motor fuels. For the month, the prices of seventeen EPI components rose, two were unchanged, and five declined.

On February 13th, the US Bureau of Labor Statistics (BLS) released Consumer Price Index (CPI) data for January 2024. The month-to-month headline CPI number rose 0.3 percent, exceeding surveys anticipating a rise of 0.2 percent. The core month-to-month CPI number increased by 0.4 percent, higher than the 0.3 percent predicted.

Within the headline CPI on a month-to-month basis, the largest increases were in shelter, food-at-home, and food-away-from-home categories. Over that same time period, from December 2023 to January 2024, the largest price declines occurred in energy prices, owing in particular to a drop in gasoline prices. In month-to-month core CPI, the largest price increases occurred within shelter, motor vehicle insurance, and medical care. Notable decreases were seen in apparel and used vehicle prices, the latter of which showed the largest monthly price decline since 1969.

January 2024 US CPI headline & core month-over-month (2014 – present)

{kind=link}

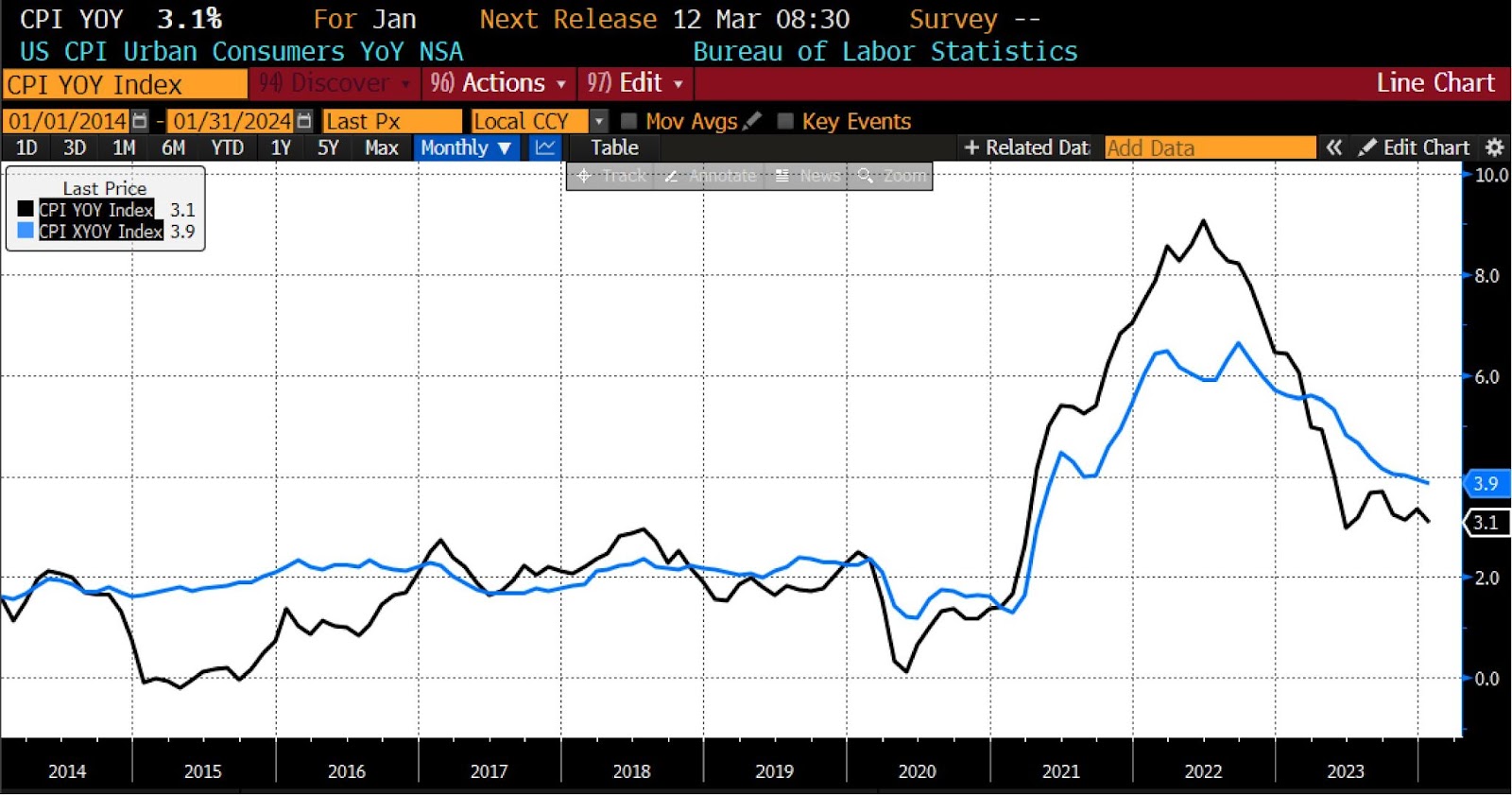

Headline CPI rose 3.1 percent from January 2023 to January 2024, higher than expectations for a 2.9 percent reading. Year-over-year core CPI rose 3.9 percent — more than expected with surveys predicting a 3.7 percent year-over-year increase.

January 2024 US CPI headline & core year-over-year (2014 – present)

{kind=link}

Over the past 12 months, the index excluding food and energy items saw a 3.9-percent increase. Within this index, the shelter component experienced a notable rise of 6.0 percent, contributing to more than two-thirds of the overall 12-month increase. Additionally, other notable increases over the same period include motor vehicle insurance (up by 20.6 percent), recreation (up by 2.8 percent), personal care (up by 5.3 percent), and medical care (up by 1.1 percent).

Historically, January tends to record some of the highest inflation readings of the year, largely due to seasonal factors. The recent positive surprise in inflation is partly attributed to volatile services categories like airfares and hotels — although airfares are not included in the Fed’s preferred inflation index (PCE). Nonetheless, the acceleration of services inflation is concerning.

The supercore measure of CPI, closely monitored by the Federal Reserve, which includes core services costs excluding housing, experienced its fastest reacceleration since May 2023. On a monthly basis, prices surged at the quickest rate since April 2022.

A small history lesson is in order. In mid-1980, core inflation hit 13.6 percent year-over-year while the Fed was already in the midst of a historic tightening campaign. Despite a recession ending in July 1981 and the Fed’s subsequent rate cuts, it wasn’t until mid-1983 that core inflation fell below 4 percent. It then rose back above 4 percent in late 1983 and stayed above 4 percent for most of the remainder of the decade, despite rate hikes in 1983, 1984, 1988, and 1989. Although the US had a largely manufacturing, goods-producing economy at that time, unlike today’s highly financialized, service-based economy, the 1980s underscore the fact that disinflation is a protracted, uneven, and uncertain process.

The January 2024 CPI report highlights the challenges of returning inflation to the Fed’s target range and suggests a bumpy road ahead. While there are still some signs of pockets of disinflationary progress, the much-anticipated rate cuts are likely delayed until June 2024.