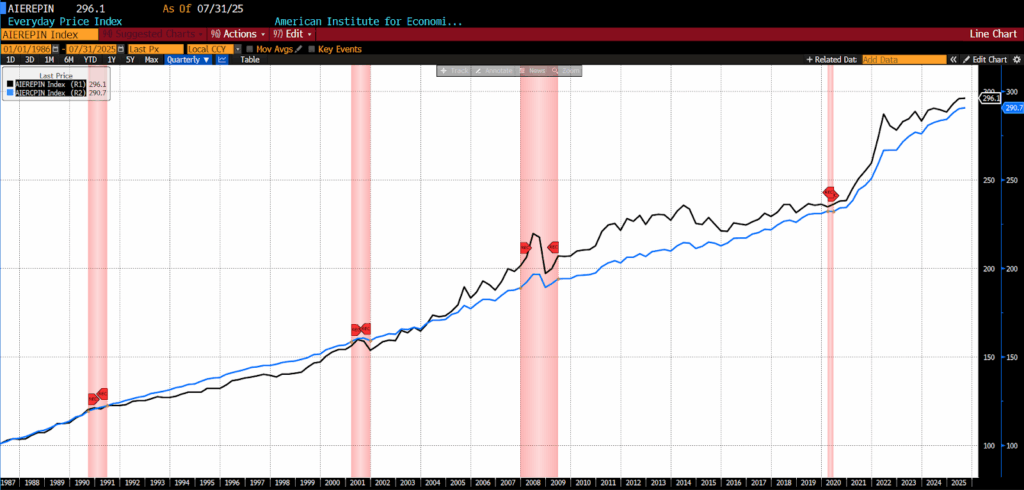

In July 2025 the AIER Everyday Price Index (EPI) rose to 296.1, a rise of 0.10 percent. This is the eighth consecutive monthly increase in the index, which has risen 1.79 percent since January 2025. Fifteen of the twenty-four components of the index saw price increases, eight saw declines, and one was unchanged.

The largest price increases this month came in the categories of gardening and lawncare, fees for lessons or instructions, and postage and delivery services. In residential telephone services, motor fuel, and cable satellite and live streaming services, price declines were steepest.

AIER Everyday Price Index vs. US Consumer Price Index (NSA, 1987 = 100)

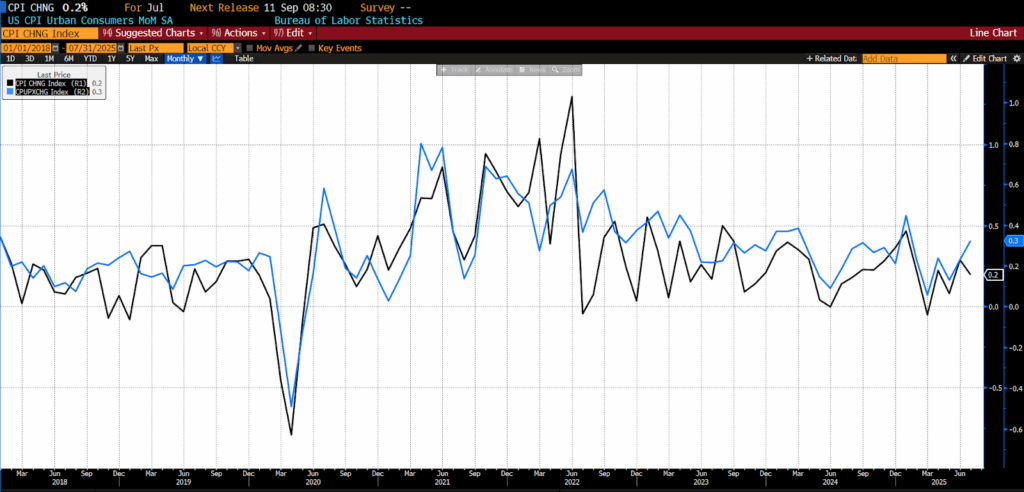

On August 12, 2025, the US Bureau of Labor Statistics (BLS) released its July 2025 Consumer Price Index (CPI) data. The month-to-month headline CPI rose 0.2 percent while the core month-to-month CPI number increased by 0.3 percent, both of which met forecasts.

July 2025 US CPI headline and core month-over-month (2015 – present)

The shelter index rose 0.2 percent in July, making it the primary contributor to the overall monthly gain. Food prices were unchanged, as a 0.3 percent increase in food away from home—driven by full-service meals (+0.5 percent) and limited-service meals (+0.1 percent)—offset a 0.1 percent decline in food at home. Within grocery categories, dairy products rose 0.7 percent, led by milk (+1.9 percent), and meats, poultry, fish, and eggs gained 0.2 percent, with beef up 1.5 percent but eggs down 3.9 percent. Offsetting declines included other food at home (-0.5 percent), nonalcoholic beverages (-0.5 percent, including a 1.3 percent drop in juices and drinks), and cereals and bakery products (-0.2 percent), while fruits and vegetables were unchanged.

The energy index fell 1.1 percent in July, reflecting a 2.2 percent drop in gasoline, a 0.9 percent decline in natural gas, and a 0.1 percent decrease in electricity. Excluding food and energy, the core index rose 0.3 percent after a 0.2 percent gain in June. Shelter components showed rent and owners’ equivalent rent both up 0.3 percent, while lodging away from home fell 1.0 percent. Medical care advanced 0.7 percent, with dental services surging 2.6 percent, hospital services up 0.4 percent, and physicians’ services up 0.2 percent, partially offset by a 0.2 percent decline in prescription drugs. Additional increases were seen in airline fares (+4.0 percent), recreation (+0.4 percent), household furnishings and operations (+0.4 percent), used cars and trucks (+0.5 percent), and personal care (+0.4 percent), while communication declined 0.3 percent and new vehicle prices were unchanged.

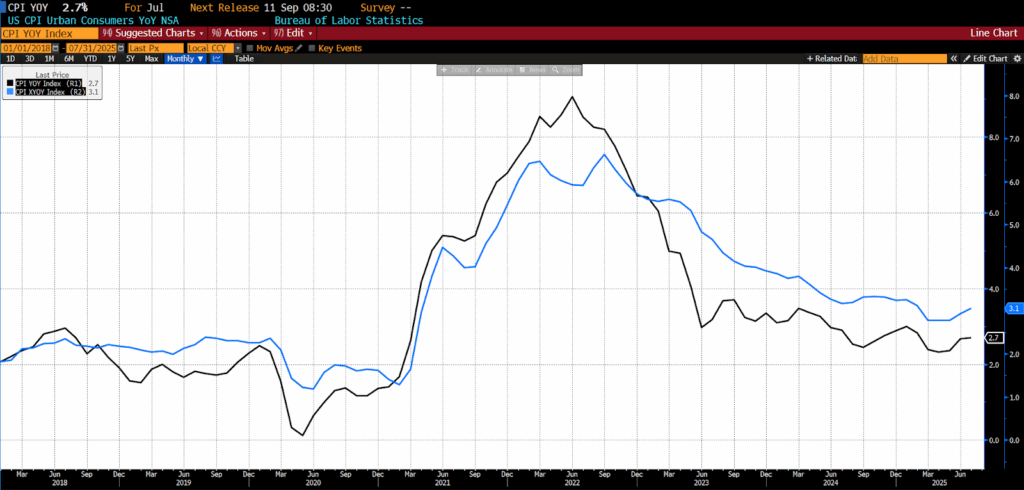

In the year-over-year data, the headline Consumer Price Index increased 2.7 percent in July 2025, slightly less than the 2.8 percent forecast. The year-over-year core index, however, was slightly hotter than anticipated, registering a 3.1 percent gain versus the expected 3.0 percent.

July 2025 US CPI headline and core year-over-year (2015 – present)

The food index increased 2.9 percent year-over-year, with food at home up 2.2 percent and notable gains in meats, poultry, fish, and eggs (+5.2 percent), including a 16.4 percent surge in eggs. Nonalcoholic beverages rose 3.6 percent, other food at home gained 1.2 percent, cereals and bakery products were up 1.0 percent, dairy products increased 1.5 percent, and fruits and vegetables edged 0.2 percent higher. Food away from home climbed 3.9 percent, led by full-service meals (+4.4 percent) and limited-service meals (+3.3 percent).

The energy index fell 1.6 percent over the year, with gasoline down 9.5 percent and fuel oil off 2.9 percent, partially offset by gains in electricity (+5.5 percent) and natural gas (+13.8 percent). Core services and goods continued to show upward pressure: shelter rose 3.7 percent year-over-year, medical care increased 3.5 percent, household furnishings and operations advanced 3.4 percent, motor vehicle insurance jumped 5.3 percent, and recreation gained 2.4 percent.

Core consumer price inflation accelerated in July to its fastest monthly pace since January, driven primarily by a rebound in services prices. Goods inflation remained subdued, with categories most exposed to tariffs showing moderated price pass-through. Interestingly, some tariff-exposed categories even posted declines (major appliances, personal computers, and apparel) while gains in items like infant apparel and photographic equipment rose substantially.

The slowdown in tariff pass-through is notable given that the US has now entered its third postponement of implementing new levies on China, potentially fostering complacency about their eventual inflationary impact. Firms appear to still be working through inventories stockpiled earlier in the year, giving them latitude to experiment with means of absorbing or mitigating tariff impacts rather than passing them directly on to consumers. Diffusion measures indicate broader core price pressures: the share of CPI components rising at an annualized pace above 4 percent climbed to 48 percent in July, up from 46 percent in June and 40 percent in May, while the share with outright declines in price fell to 27 percent from 33 percent last month. These dynamics highlight that lag effects remain a key factor — policy actions, whether interest rate changes or trade measures, filter through the economy unpredictably and with varying intensity across sectors.

Market reaction to the CPI release reflected both the firmness of the data and evolving macro risks. Fed funds futures now imply roughly 24 basis points of easing in September and a cumulative 62 basis points by year-end, undoubtedly incorporating the recent, massive downward revision to nonfarm payrolls into the calculus of the Fed’s decision-making. The persistence of service-sector inflation, even as goods prices cool, complicates Powell & Company’s path: while tariff-related pressures have moderated for now, the combination of broadening price gains, lagged policy effects, and a still-softening labor market leaves the timing, scale, and certainty of future rate cuts very much in play.