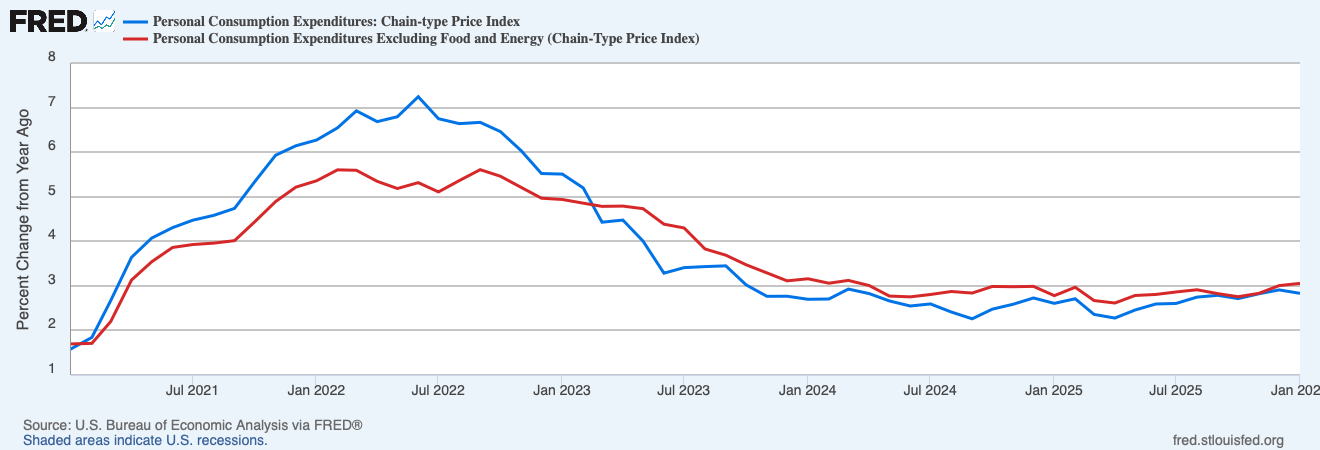

Inflation ticked down in January, the latest data released Friday from the Bureau of Economic Analysis shows. But it still remains well above the Federal Reserve’s target. The Personal Consumption Expenditures Price Index (PCEPI), which is the Fed’s preferred measure of inflation, grew at an annualized rate of 3.4 percent in January 2026, down from 4.4 percent in the last month of 2025. The PCEPI grew at an annualized rate of 3.5 percent over the prior three months and 2.8 percent over the prior year.

Core inflation, which excludes volatile food and energy prices, remained elevated. Core PCEPI grew at an annualized rate of 4.5 percent in January 2026. It grew at an annualized rate of 3.7 percent over the prior three months and 3.1 percent over the prior year.

Breaking It Down

The conventional view is that tariffs have pushed up prices over the last year. If that were the case, we would expect goods prices to grow much faster than services prices. It is easier to import a hat than a haircut, and tariffs will generally cause both foreign and domestic hat producers to raise their prices. Foreign hat producers raise their prices to cover some portion of the tariff. Domestic hat producers raise their prices because they know foreign hat producers will not be able to underbid them given the tariff.

Goods prices grew at an annualized rate of 0.5 percent in January, and were up 1.3 percent year-over-year. For comparison, goods prices grew at an average annualized rate of -0.1 percent per year. That suggests goods prices have grown about 1.4 percentage points faster than usual over the last year.

Services prices grew at an annualized rate of 4.6 percent in January, and have grown 3.5 percent over the last year. Over the five-year period just prior to the pandemic, services prices grew at an average annualized rate of 2.3 percent per year. Hence, services prices have grown about 1.2 percentage points faster than usual over the last year. Moreover, the excess growth of services prices can no longer be explained by the housing component, which tends to lag broader price movements. Housing prices grew 3.2 percent over the last year, which is around 10 basis points slower than observed over the five-year period just prior to the pandemic.

Although goods prices have grown a bit faster than services prices, the difference — just 20 basis points — is relatively small. Recall that headline PCEPI inflation is around 80 basis points above the Fed’s two-percent goal. The available evidence suggests that inflation is relatively widespread. It is not primarily due to the tariffs.

Competing Objectives

Elevated inflation is just one of the concerns Fed officials will be discussing at this week’s Federal Open Market Committee meeting. They are also concerned about the relatively slow job growth observed over the last year.

“There is no dismissing the weakness of job creation in 2025,” Fed Governor Christopher Waller said last month. Data released since then would seem to confirm his fears that the strong January “report may contain more noise than signal.” The economy lost 92,000 jobs in February, nearly wiping out the outsized gains in January.

Congress has tasked the Fed with delivering price stability and maximum employment. But it has largely left it to the Fed to determine what those terms mean and how to balance the two goals when they are in conflict.

The Fed explains how it will deal with diverging goals in its 2025 Statement on Longer-Run Goals and Monetary Policy Strategy:

The Committee’s employment and inflation objectives are generally complementary. However, if the Committee judges that the objectives are not complementary, it follows a balanced approach in promoting them, taking into account the extent of departures from its goals and the potentially different time horizons over which employment and inflation are projected to return to levels judged consistent with its mandate. The Committee recognizes that employment may at times run above real-time assessments of maximum employment without necessarily creating risks to price stability.

The so-called “balanced approach” would seem to suggest it will place equal weight on the two goals. But the “extent of departures” and “different time horizons” affords a lot of flexibility. And the special attention given to employment in the last line suggests the Fed might put more weight on employment in practice.

What Should Be Done?

My own view is that the economy is at or near full employment at the moment, with low job growth reflecting demographic changes and increased immigration enforcement. If I am correct, the Fed should not worry about the labor market. Instead, it should focus on getting inflation back down to target. The Iran conflict may complicate the Fed’s job, by adding temporary supply-driven inflation (which it should ignore) to the permanent demand-driven inflation seen in the January release (which it should address). If supply-driven inflation emerges, and I suspect it will, the Fed will need to parse the data carefully in order to determine the extent of the inflation problem and, correspondingly, the extent to which it should respond to above-target inflation.

It is highly unlikely that Fed officials will adjust their policy rate on Wednesday. The CME Group currently puts the odds at just 0.9 percent. But one should pay close attention to what Fed officials signal in their post-meeting statement and what Chair Powell tells the press. That may give us a better sense of how Fed officials are interpreting the incoming data — and what they intend to do about it.