Washington has a habit of changing its budget goals — not because the country solved the spending-driven debt problem, but because each goal proved harder than lawmakers were willing to confront.

I remember working on fiscal policy in 2011, when lawmakers still talked about balancing the budget. It was an intuitive target. If the government only spent what it collected in revenues, the debt problem would eventually disappear.

Simple in theory. Difficult to achieve in practice.

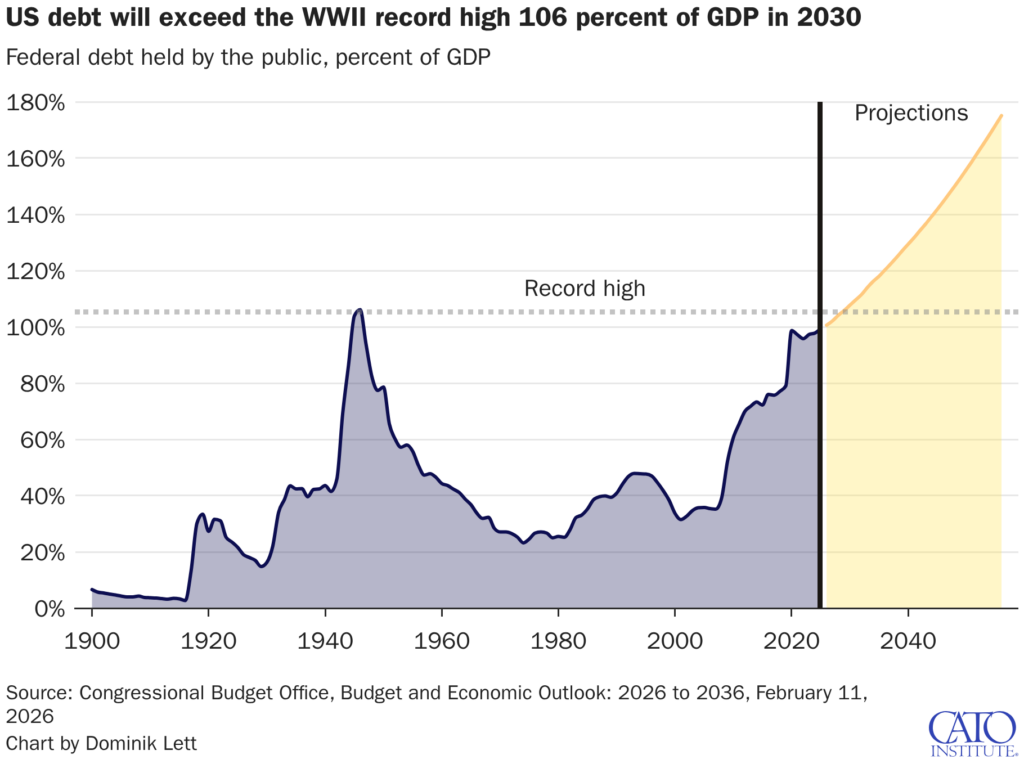

So the focus shifted to stabilizing the debt. When debt began approaching 100 percent of GDP in 2020 — as spending kept climbing and interest costs began growing steeply — balancing the budget looked increasingly unattainable.

Republicans kept up appearances for a while longer, inflating economic growth expectations in their budget plans to make up for a lack of fiscal restraint. If you can’t balance the budget honestly, maybe you can fake it? At least they tried to make the numbers work, albeit by invoking fiscal fantasies.

Now there is a new goalpost: limiting deficits to three percent of GDP. As House Budget Committee Chairman Jody Arrington (R-TX) recently stated on CNBC’s Squawk Box, following a congressional hearing to discuss the new target:

We’ve been looking at 10-year balanced budgets for decades. And we haven’t had a balanced budget in a quarter of a century. Today, if we’re going to balance in 10 years — that’s $18 trillion. We’d have to do what we did in the Big Beautiful Bill every year for 10 years.

So, I think any successful endeavor starts with defining success and setting achievable — ambitious — but achievable goals.

And in this case, we’re talking about reframing where we take our crisis level annual deficits per economic output, which is about six percent of GDP, and put it on a glide slope down to three percent — here we’re growing the economy faster than our rate of deficit spending and inflation. That should put us on a better trajectory, a more sustainable one. And then, we can take it from there on a more ideal path to balance.

Arrington is right that setting an achievable goal matters. We should also be clear about what this new goal represents.

A deficit-to-GDP target is no more — or less — arbitrary than any other fiscal benchmark short of balance. There is nothing inherently magical about three percent. It is not a law of economics. It is a political and analytical compromise.

For years, New Keynesian economists have argued that governments do not need to balance their budgets, only to keep deficits at a level consistent with a stable, or even slowly rising, debt burden, so long as the interest rate on public debt remains below the economic growth rate. This politically convenient argument was lauded in academic and government circles. How swell to have cover to continue growing the debt burden on younger generations because “the economists” said it was OK to do so.

But “sustainable” was never meant to suggest “unlimited.”

In that sense, the three percent target may be more honest than what came before. It acknowledges that the United States is not on a path to balance anytime soon and sets a minimum condition for avoiding further deterioration.

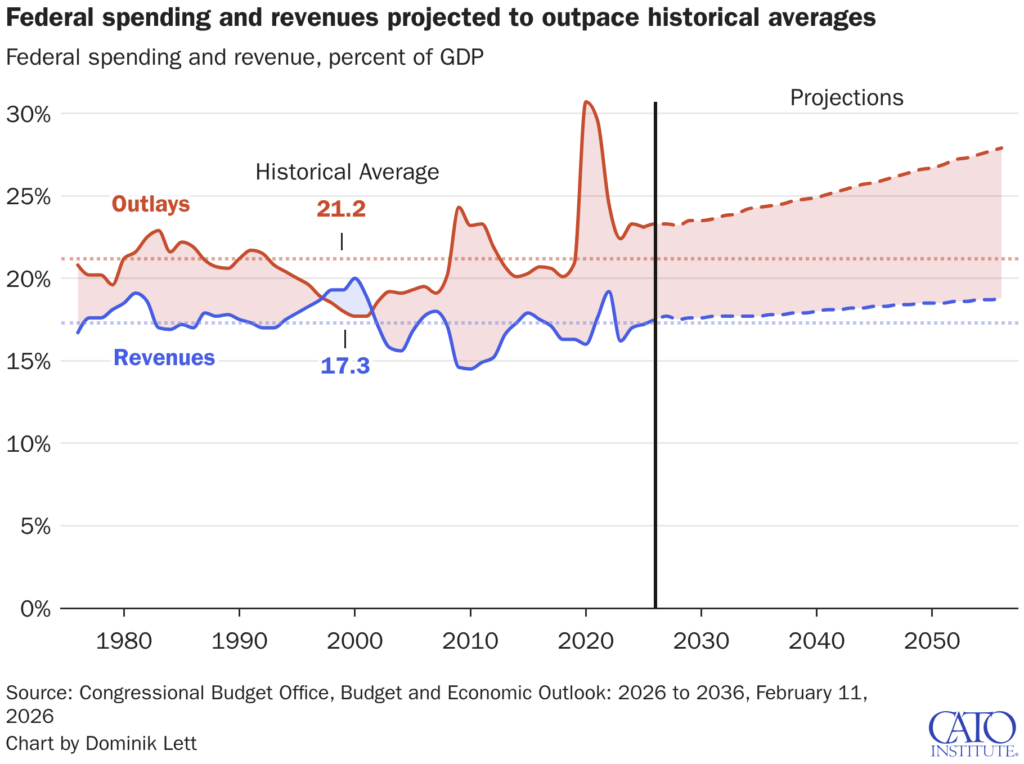

This is important if we can finally achieve bipartisan recognition that current deficits — growing from six percent of GDP to nine percent annually over the next few decades — are unsustainable. As discussed in the recent House Budget Committee hearing, reducing deficits to three percent of GDP would roughly stabilize the debt at today’s already elevated levels. It could stop the debt from growing even bigger as a share of the economy. That’s critical.

And yet even this goal demands far more political will than Congress has demonstrated. The scale of the adjustment is significant. Bringing deficits down to three percent of GDP would require roughly $10 trillion in deficit reduction over the next decade.

That is the real test. Can Congress agree on a target and make the necessary fiscal adjustments to achieve it?

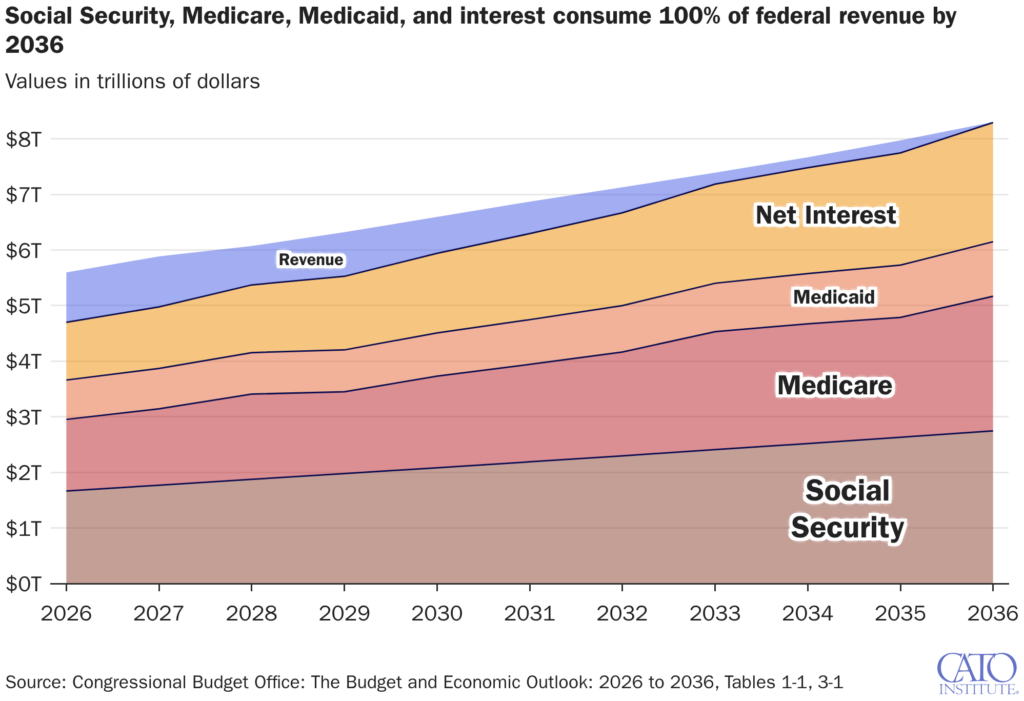

Because the urgency to rein in the growth of US debt is no longer abstract. The United States has now been downgraded by all three major credit rating agencies. Interest costs are rising rapidly and already rival spending on national defense. Looking ahead, the federal government’s largest obligations — Social Security, Medicare, Medicaid, and interest on the debt — are projected to consume all federal revenues within little more than a decade. At that point, every other government function — from national defense to infrastructure to basic operations — would have to be financed with borrowed money.

Something has to give. And that is where Congress consistently falls short.

Most federal spending operates on autopilot. Mandatory programs — primarily Social Security, Medicare, and Medicaid — make up the bulk of the budget and are rarely revisited in any comprehensive way. Lawmakers barely even debate discretionary spending anymore, and Republicans have increasingly turned to mandatory spending to fund portions of defense and immigration enforcement.

Following the deficit-increasing One Big Beautiful Bill Act from July 2025, Congress is again considering budget reconciliation — this time in part to finance additional military spending related to the conflict with Iran and to circumvent Democratic opposition to funding ICE.

Reconciliation could provide an opportunity to enact broader fiscal reforms, including reducing spending on major entitlement programs. The growth in Medicaid and food stamp spending, for example, was slowed in the latest reconciliation bill, in part framed as an effort to reduce waste, fraud, and abuse. Those are legitimate concerns. Yet even eliminating fraud would not come close to arresting the growth in spending and debt.

Without significant changes to health care programs and Social Security — the largest drivers of rising government debt — the pattern will repeat. Congress will announce targets, defer them, and eventually replace them.

Congress does not lack warnings. Interest costs are rising, debt is growing faster than the economy, and fiscal space is shrinking. The question is whether lawmakers will treat the three percent target as a turning point — or as the next step in lowering expectations.